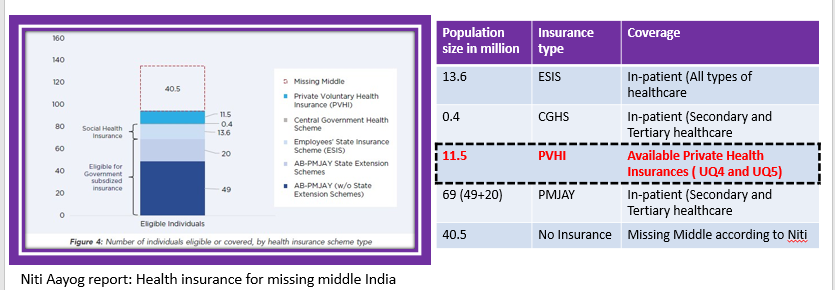

This is the picture of India’s Health Insurance considering Health Insurance as a fundamental need provided users find value, suitability, and affordability.

- The bottom 40% of the population are the beneficiaries of the State-Sponsored Health Insurance Scheme - PMJAY.

- The top 60% of the population is left to be insured by Private Players.

- And if you look at the above chart the available Health Insurance are suitable and affordable for around 11.5% - Private Voluntary Health Insurance (PVHI).

This left a void the be filled by new-age companies to build products for the missing middle (50%), and, certainly, available health insurance is not going to make any dent in the missing middle because those insurance are neither affordable nor suitable but why?

Even though I have written this from the missile middle POV, it is relevant for the PVHI as well. So, the stream that deals with the underwriting insurance risk is called “Actuarial Science and Risk Management”.

To begin with, even the available Health Insurance for the top 10% of the population is one size fits all and there are various problems with the way Insurance manufacturers are underwriting risk but I will keep my temptation to not go into that part and focus on the missing middle. To keep this post shorter, in underwriting insurance there could potentially be 12 types of risk a manufacturer would like to evaluate to measure the risk and assign the premium.

- Genetic

- Medical Conditions

- Chronic

- Acute

- Occupational Factor

- Social and Economic factors

- Psychosocial factors

- Vaccination Status

- Access of Healthcare

- Environment

- Lifestyle

- Lifestage

- Past Medical History

- Habits

I am sure many of you must have purchased Health Insurance how many of the risk manufacturers or brokers evaluate at the time of writing the insurance? Let’s keep the evaluation of all risks aside, I am sure, you must have been asked questions, by underwriters, such as Past Medical History, Habits, Lifestyle etc. Do you know most of the Health Insurance claim rejections are due to the above because policyholders, at the time of purchasing Health Insurance, create Information asymmetry because there is no tool by which objectively, the above risk could be evaluated at the time of writing insurance.

There are multiple root causes behind one-size-fits-all and inefficiency in Health Insurance, however, two of them are

- Treating Healthcare and Health Insurance separately

- Treating Health Insurance as a yearly business

Let’s take one example from the above risk list - Genetic. An insurer insuring parents from a family is actually unlocking a future Genetic risk, if any, of their children. And can be taken as a reference to make Insurance personalized and affordable.

All the above problems exist for PVHI but that will be solved by an ecosystem. However, when we talk about the missing middle using a wedge to enter the market and have control of one component can make Health Insurance suitable and affordable for 500 million and this will unlock INR 1,25,000 Cr.

This is a small part of the essay I wrote on my blog, you can read it here ![]()