- Byrne Hobart had a nice yet seemingly obvious framing of a CEO’s job as a capital allocator. Part of the CEO’s job is deciding on whether to spend money on NFTs or building a new feature that will attract more users. Given that all decisions are made under uncertainty, capital allocation decisons are never easy.

Good capital allocators also have to be ruthlessly accurate at assessing their company’s own strengths. The more distant a capital allocation decision is from just scaling up the core business, the more other companies could conceivably do exactly the same thing. For example, if a company is getting into some new industry, it has to either explain why it’s going to be more profitable than incumbents or why the incumbents are going to be more profitable in the future—because shareholders already have the option to allocate capital into that industry, by selling their stock and investing in the incumbents.

https://capitalgains.thediff.co/p/ceo-capital-allocator

Pair this with Michael Mauboussin and Dan Callahan’s treatise on the same topic:

Creating value ought to be an imperative for at least two reasons. The first is competition. A firm that does a poor job of managing its resources will lose in the marketplace to a company that is managed better. The second is consideration of the opportunity cost of capital. Companies have to explicitly acknowledge that all capital has an opportunity cost, the rate of return they could earn on the next best alternative. Capital that fails to earn the cost of capital over the long term destroys value and imperils a company’s prospects for prosperity.

The researchers in fact found an optimal degree of reallocation. But they also discovered that only 38 of the 5,760 observations, or less than 1 percent, were above that threshold. In other words, the vast majority of companies could improve their financial performance by increasing their reallocation.

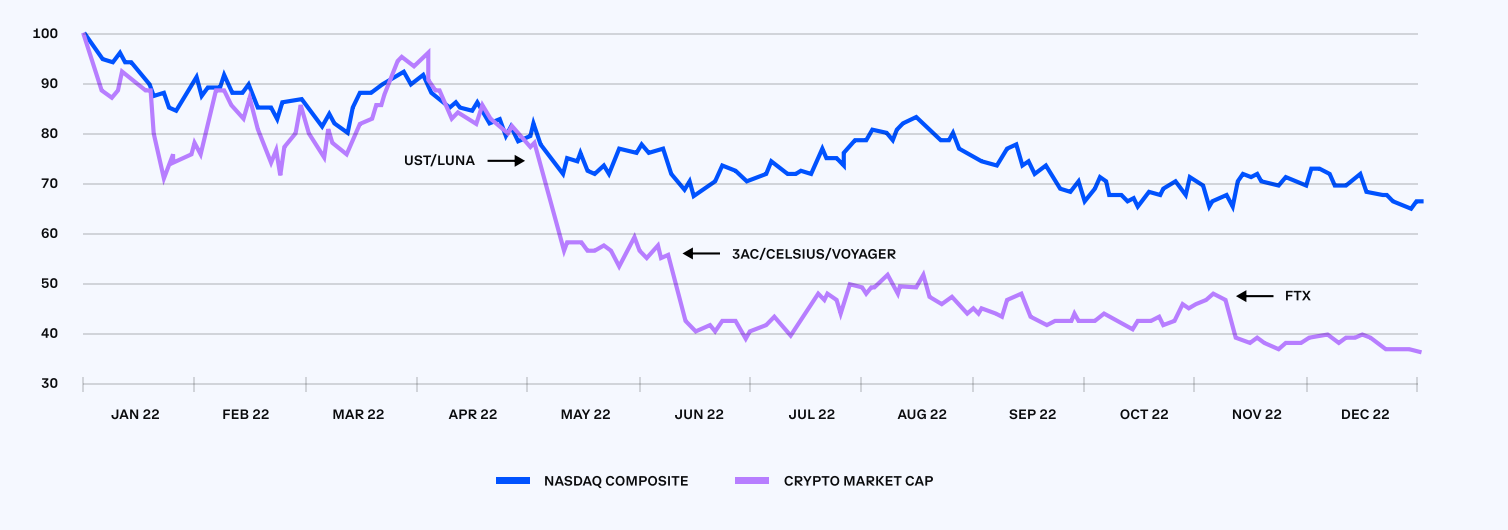

- When Gary Gensler became the chairman of the SEC, the crypto industry was cautiously optimistic. They figured since Mr. Gensler had taught a MIT course on Blockchain tech, he would be pro-crypto, but their hopes were immediately dashed. In August 2021, he gave a speech at the Aspen Security Forum which foreshadowed what would come:

This asset class is rife with fraud, scams, and abuse in certain applications. There’s a great deal of hype and spin about how crypto assets work. In many cases, investors aren’t able to get rigorous, balanced, and complete information.

There’s actually a lot of clarity on that front. In the 1930s, Congress established the definition of a security, which included about 20 items, like stock, bonds, and notes. One of the items is an investment contract.

He kept reiterating that existing US securities laws were more than adequate and that new rules weren’t required. Apart from the regular soundbites, the SEC didn’t make a lot of moves, but all that has changed in the last 12 months. The SEC had gone on the offensive, bringing a series of enforcement actions that have led the industry to denounce the regulation by enforcement instead of formulating new crypto-specific laws. These new lawsuits and enforcement actions are making matters worse for an industry that’s facing existential questions after a ~50% decline in marketcap

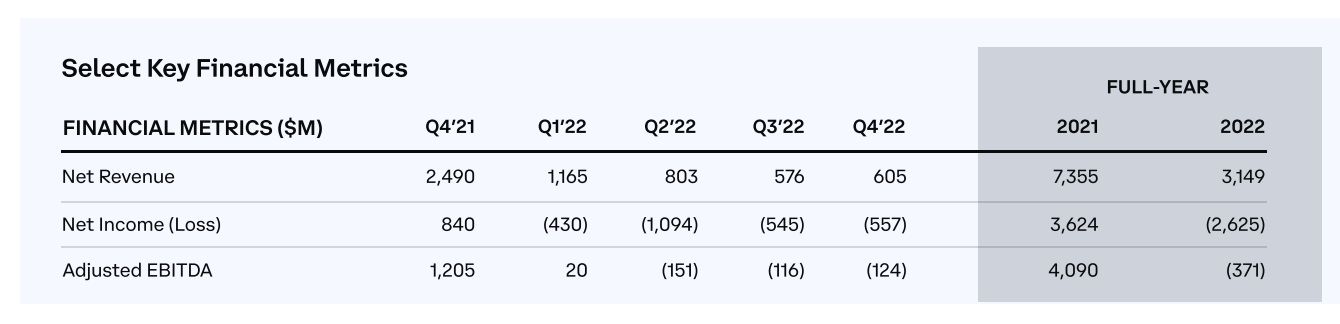

Take a look at Coinbase results:

Coindesk published a good summary of SEC’s newfound appetite for bringing enforcement actions against major crypto players like Kraken, Coinmase Gemini, and Terra Luna:

https://www.coindesk.com/policy/2023/02/21/secs-shadow-crypto-rule-taking-shape-as-enforcement-cases-mount/

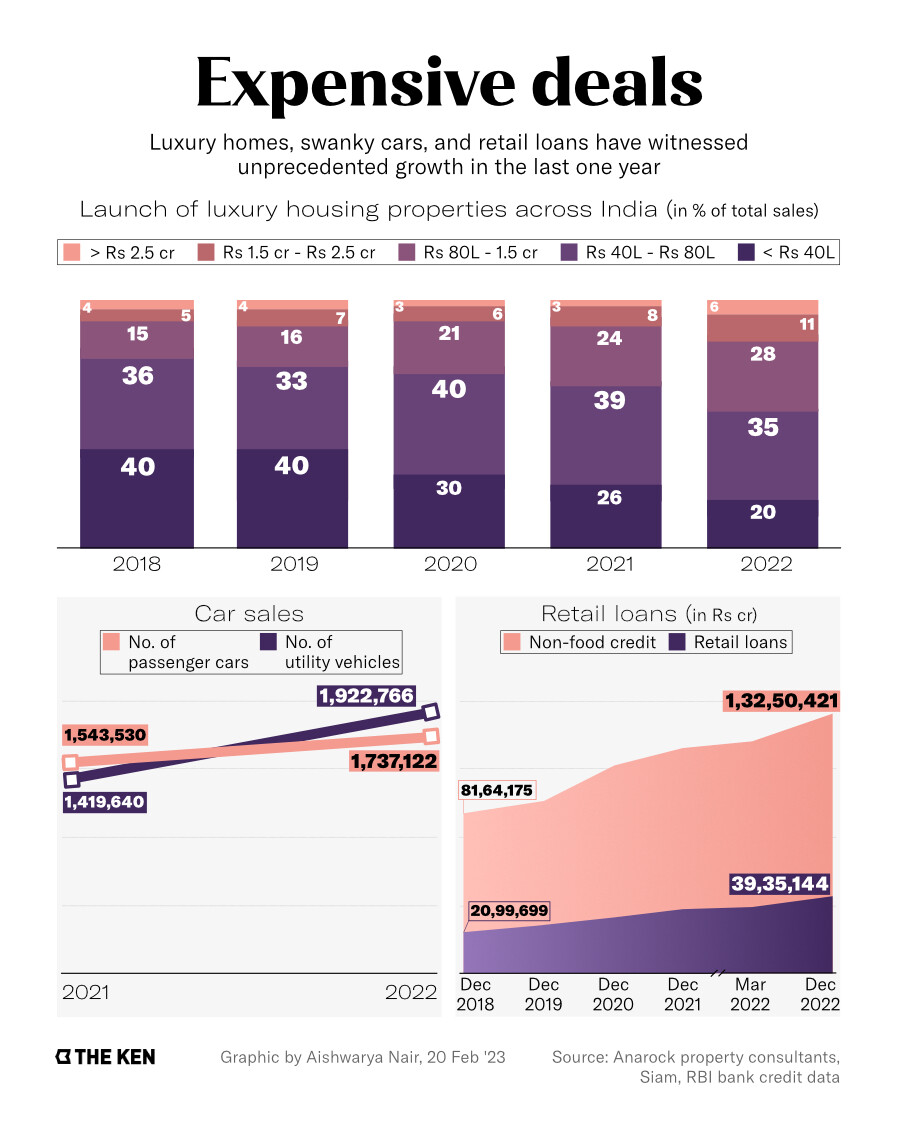

- The-Ken published an interesting piece on the recent recovery in the credit cycle. The record rise in borrowing by individuals has led to increase sales of pricey apartments,

“Sales of apartments priced over Rs 1.5 crore (US$181,300) doubled in 2022 in India. Luxury projects priced above Rs 2.5 crore (US$302,000) in tier-1 cities are getting sold out at the pre-launch stage. Inventory overhang for such projects is at a decadal low,” said a senior employee at JLL India, a real-estate services company. They did not want to be named as they were not authorised to speak with the media, and the data is not public.

Luxury-car sales have also surged as more and more young Indians flock to showrooms. Mercedes Benz’s most basic model costs Rs 72 lakh (~US$87,000). Still, footfall almost doubled in 2022 for Mercedes Benz, BMW, and Audi, said the dealers of all three companies. They also said that the average age of customers would now be around 35, compared to 45 just a few years ago. They did not want to be named as they were not authorised to speak with the media.

- The acquisition of ZestMoney by PhonePe is still pending several months after the announcement.

https://themorningcontext.com/internet/inside-phonepes-pay-now-buy-later-deal-with-zestmoney

Pair this with:

https://www.medianama.com/2023/02/223-rbi-faqs-digital-lending-guidelines/

- The rise of target maturity funds has been one of the more interesting development in the Indian fixed income space. This is all the more relevant given the rise in interest rates. Target maturity funds are similar to fixed maturity plans. All target maturity funds are index funds and each fund has a defined maturity. After the maturity, you get back the money, just like a bond.

There are several advantages of target maturity funds over direct bonds and fixed deposits:

- Higher yields

- Tax-efficient. STC < 3 years and LTCG with indexation > 3 years.

Interest on FDs above Rs 40,000 is taxed at your slab rate and there’s a TDS of 10%>

Interest income from bonds is taxed at slab rates. - Retail friendly given that they are easier to understand compared to single bonds and also more diversified given that target funds are diversified basket of bonds.

In the last 4-5 of years, there has been growing interest (to the extent that VCs care about capital markets ![]() ). The attraction has been the growing retail interest in high-yield products. But as things stand, target maturity funds are vastly superior and safer compared to individual bonds and structured high-yield funds. The yield differential has also shrunk significantly. But today, 99.9% of the AUM in target maturity funds is from institutions and HNIs. Will be interesting to see how this plays out in the long run.

). The attraction has been the growing retail interest in high-yield products. But as things stand, target maturity funds are vastly superior and safer compared to individual bonds and structured high-yield funds. The yield differential has also shrunk significantly. But today, 99.9% of the AUM in target maturity funds is from institutions and HNIs. Will be interesting to see how this plays out in the long run.

From SEBI

- Advisory for SEBI Regulated Entities (REs) regarding [Cybersecurity best practices]. (SEBI | Advisory for SEBI Regulated Entities (REs) regarding Cybersecurity best practices)

- Consultation Paper on Regulatory Framework for ESG Rating Providers (ERPs)

Chart of the day

US venture capital (VC) funds raised

WSJ